Executive Summary

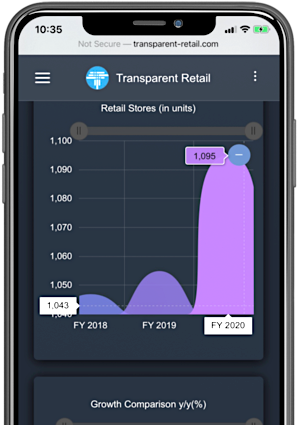

Haverty Furniture Companies, Inc. operates as a specialty retailer of residential furniture and accessories in the United States. The company offers furniture merchandise under the Havertys brand name. It also provides custom upholstery products; and mattress product lines under the Sealy, Tempur-Pedic, Serta, Stearns & Foster, Beautyrest Black, and Scott Living names, as well as private label Skye name. The company sells home furnishings through its retail stores, as well as through its Website. As of April 01, 2020, it operated 120 showrooms in 16 states in the Southern and Midwestern regions. Haverty Furniture Companies, Inc. was founded in 1885 and is headquartered in Atlanta, Georgia.

STRENGTHS

WEAKNESSES

SIMILAR COMPANIES

TICKER: BBBY

TICKER: CONN

TICKER: TCS

1Margins

Is Haverty Furniture Companies, Inc. profitable compared to industry average?

Analysis Check: 6/6

1.1Gross Margin (%)

- Outperformed : Generated higher Gross Margin (56%) in FY 2020, compared to the median of its peer group (42.5%).

| For the period ended | Company | Industry |

|---|---|---|

1.2EBITDA Margin (%)

- Outperformed : Generated higher EBITDA Margin (12.7%) in FY 2020, compared to the median of its peer group (7.3%).

| For the period ended | Company | Industry |

|---|---|---|

1.3Net Margin (%)

- Outperformed : Generated higher Net Margin (7.9%) in FY 2020, compared to the median of its peer group (2.3%).

| For the period ended | Company | Industry |

|---|---|---|

1.4Gross Margin Growth (YoY)

- Positive : Gross Margin(%) expanded by 3.4% YoY in FY 2020.

| For the period ended | Company | Industry |

|---|---|---|

1.5EBITDA Margin Growth (YoY)

- Positive : EBITDA Margin(%) expanded by 111.6% YoY in FY 2020.

| For the period ended | Company | Industry |

|---|---|---|

1.6Net Margin Growth (YoY)

- Positive: Net Margin(%) expanded by 190.1% YoY in FY 2020.

| For the period ended | Company | Industry |

|---|---|---|

2Financial Health

How is HVT’s financial position?

Analysis Check: 5/6

2.1Financial Position Analysis

- STA/STL (1.55x): Short Term Assets ($316.24 million) exceeded Short Term Liabilities ($204.04 million) in FY 2020.

- STA/LTL :There was no Long Term Liabilities during the period.

| For the period ended | Company | Industry |

|---|

2.2Debt to Equity Analysis

- Debt/Equity (0) : Though Debt ($0 million) to Equity ($252.97 million) ratio (0x) in FY 2020 was not within the acceptable range but was below the median of its peer group (0.49x).

| For the period ended | Company | Industry |

|---|

2.3Cash Conversion Cycle (in Days)

- At Par : Reported a Cash Conversion Cycle of 0 days in FY 2020, at par with the median of its peer group (77 days).

| For the period ended | Company | Industry |

|---|---|---|

2.4Interest Coverage Ratio (x)

- Outperformed : Interest Coverage Ratio (195.92x) in FY 2020 was above the minimum acceptable ratio and was above the median of its peer group (18.1x).

| For the period ended | Company | Industry |

|---|---|---|

2.5Total Liquidity to Short Term Liability

- Total Liquidity/STL (1.06) : Total Liquidity ($215.36 million) exceeded Short Term Liabilities ($204.04 million) in FY 2020.

| For the period ended | Company | Industry |

|---|

3Cash Flow Management

What is the HVT’s debt servicing capability?

Analysis Check: 5/6

3.1Cash Flow From Operations Growth (YoY)

- Outperformed : Cash Flow from Operations expanded by 105.29% YoY in FY 2020.

| For the period ended | Company | Industry |

|---|---|---|

3.2Free Cash Flow Growth (YoY)

- Outperformed : Free Cash Flow expanded by 156.05% YoY in FY 2020.

| For the period ended | Company | Industry |

|---|---|---|

3.3Cash Flow From Operations

- Outperformed: Debt ($0 million) to CFO ($130.19 million) ratio (0x) in FY 2020 was below the median of its peer group (0.75x).

- Underperformed: CFO ($130.19 million) to CAPEX ($10.93 million) ratio (11.91x) in FY 2020 was above the median of its peer group (3.93x).

- Outperformed: Cash Fixed Charge Coverage ratio (3.54x) in FY 2020 was above the minimum acceptable ratio and was above the median of its peer group (2.47x).

| For the period ended | Company | Industry |

|---|

3.4Free Cash Flow (FCF) / Sales

- Outperformed: FCF to Sales ratio (0.16x) in FY 2020 was above the median of its peer group (0.08x).

| For the period ended | Company | Industry |

|---|---|---|